A first house financing strategy is more than just securing a mortgage. It’s about structuring your purchase in a way that balances affordability, flexibility, and long-term financial stability.

For first-time buyers, having a clear strategy early on can help avoid common pitfalls and make the entire process more predictable.

What Is a First House Financing Strategy

A first house financing strategy is a plan that outlines how you will fund your home purchase, manage ongoing costs, and align the decision with your broader financial goals.

It typically includes:

- Down payment planning

- Loan type selection

- Budgeting for monthly payments

- Managing closing and upfront costs

Instead of reacting to lender options, a strategy helps you stay in control of the process.

Understanding Your Financing Options

Before choosing a mortgage, it’s important to understand the main loan types available.

| Loan Type | Key Feature | Best Fit |

|---|---|---|

| Conventional Loan | Standard qualification | Strong credit profiles |

| FHA Loan | Lower credit requirements | First-time buyers |

| VA Loan | No down payment (eligible borrowers) | Military members |

| USDA Loan | Rural property focus | Specific geographic areas |

Each option comes with different requirements, costs, and flexibility levels.

Pro Insight

The “best” loan isn’t always the one with the lowest interest rate. Flexibility, lower upfront costs, and manageable monthly payments can sometimes provide more long-term value.

How to Build a Smart Financing Plan

Creating a solid strategy involves a few key steps.

- Set a realistic budget

Focus on what you can comfortably afford, not just what you qualify for - Plan your down payment

Balance upfront cost with monthly affordability - Factor in total monthly expenses

Include taxes, insurance, and maintenance - Secure mortgage pre approval

This clarifies your buying range and strengthens your position

These steps create a foundation that supports confident decision-making.

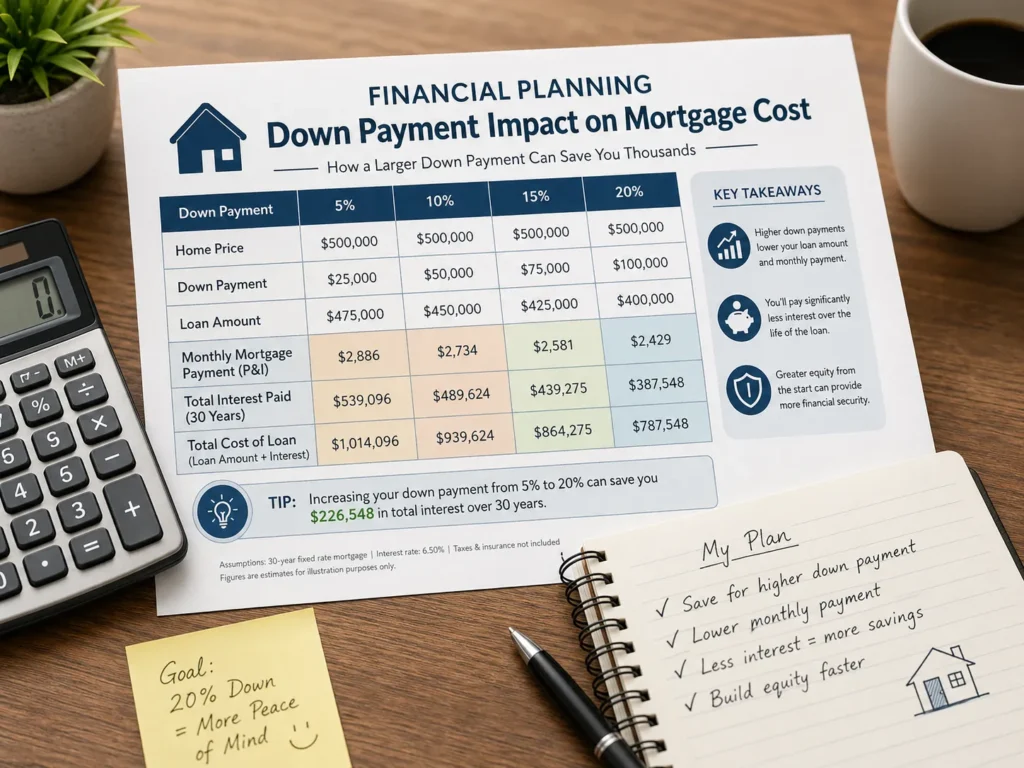

Down Payment Strategy

The size of your down payment directly affects your loan and monthly payments.

- Higher down payment → lower monthly cost and interest

- Lower down payment → more cash flexibility but higher payments

Some buyers choose to keep more cash on hand for emergencies instead of putting everything into the home. This balance is often more practical than maximizing the down payment.

Quick Tip

Avoid using all your savings for the down payment. Keeping a financial cushion for unexpected expenses can make homeownership more sustainable.

Managing Monthly Affordability

Your monthly payment is one of the most important parts of your financing strategy.

It typically includes:

- Principal and interest

- Property taxes

- Homeowners insurance

- Potential mortgage insurance

A common guideline is to keep housing costs within a manageable portion of your income, leaving room for other financial goals.

Fixed vs Adjustable Rate Strategy

Choosing between fixed and adjustable-rate mortgages can influence long-term costs.

| Feature | Fixed Rate Mortgage | Adjustable Rate Mortgage |

|---|---|---|

| Interest Stability | Consistent | Changes over time |

| Initial Rate | Higher | Often lower |

| Predictability | High | Moderate |

| Risk Level | Lower | Higher |

| Best For | Long-term stability | Short-term ownership plans |

Your timeline and risk tolerance should guide this decision.

Real World Scenario

Consider a first-time buyer with steady income and moderate savings.

They choose:

- A manageable down payment rather than the maximum possible

- A fixed-rate mortgage for stability

- A monthly payment well within their budget

This approach allows them to handle unexpected costs without financial strain, even if it means slightly higher interest over time.

Common Financing Mistakes to Avoid

Even with a strategy, it’s easy to make missteps.

- Stretching the budget too far

- Ignoring total ownership costs

- Choosing a loan based only on interest rate

- Failing to compare multiple lenders

Avoiding these mistakes can improve both short-term comfort and long-term outcomes.

Frequently Asked Questions

What is the best financing option for a first house

It depends on your financial profile, but FHA and conventional loans are common starting points for first-time buyers.

How much should I put down on my first home

Down payments vary, but many buyers put between 3% and 20%, depending on loan type and financial goals.

Is pre approval necessary

It’s not mandatory, but it helps define your budget and strengthens your offer when buying a home.

Should I choose fixed or adjustable rate

Fixed rates offer stability, while adjustable rates may provide lower initial costs but come with more uncertainty.

How do I know what I can afford

A combination of income, expenses, and financial goals helps determine a realistic budget beyond lender approval limits.

Conclusion

A well-planned first house financing strategy can make the difference between a stressful purchase and a sustainable investment. By focusing on affordability, flexibility, and long-term goals, you can create a plan that supports both your homeownership journey and your overall financial health.

Taking the time to build a thoughtful strategy now can lead to more confident decisions and fewer surprises later.

https://www.consumerfinance.gov

https://www.hud.gov

https://www.usa.gov/housing-help

https://www.fhfa.gov

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.