Understand refinance closing costs, what they include, how much they cost, and when refinancing actually saves money.

Refinancing can lower your monthly payment or shorten your loan term—but refinance closing costs often catch homeowners off guard. These fees can quietly erase savings if you don’t know what to expect or how to evaluate them properly.

The good news? With the right perspective, closing costs become a decision tool—not a deal breaker.

What Refinance Closing Costs Actually Are

Refinance closing costs are fees paid to process and finalize a new mortgage loan. They’re similar to purchase closing costs, but typically lower because there’s no property transfer.

In real life, this might look like a homeowner excited about dropping their rate—only to pause when they see several thousand dollars due at closing. Those costs don’t mean refinancing is bad; they just need to be weighed correctly.

What’s Commonly Included in Refinance Costs

Most refinance closing costs fall into predictable categories:

Loan origination and underwriting

Appraisal and credit report fees

Title search and lender’s title insurance

Recording and administrative fees

Prepaid interest and escrow adjustments

Some lenders bundle these differently, which is why comparing offers side by side matters more than focusing on one single fee.

Average Refinance Closing Costs Compared

| Cost Category | What It Covers | Typical Range | Paid To |

|---|---|---|---|

| Origination Fee | Loan processing | 0.5%–1% of loan | Lender |

| Appraisal | Property valuation | $300–$600 | Appraiser |

| Title Services | Ownership verification | $500–$1,500 | Title company |

| Recording Fees | Legal filing | $50–$300 | Local government |

| Prepaid Items | Interest & escrow | Varies | Lender |

Seeing costs grouped like this makes it easier to judge whether a quote is reasonable—or inflated.

Paying Closing Costs Upfront vs Rolling Them In

Some homeowners pay closing costs in cash at closing. Others choose a “no-closing-cost” refinance, where fees are rolled into the loan or offset by a slightly higher interest rate.

Neither option is automatically better. Paying upfront may maximize long-term savings, while rolling costs in can preserve cash flow. The smarter choice depends on how long you plan to keep the loan.

A homeowner planning to move in three years may benefit from minimal upfront costs, while a long-term owner may prefer the lowest possible rate.

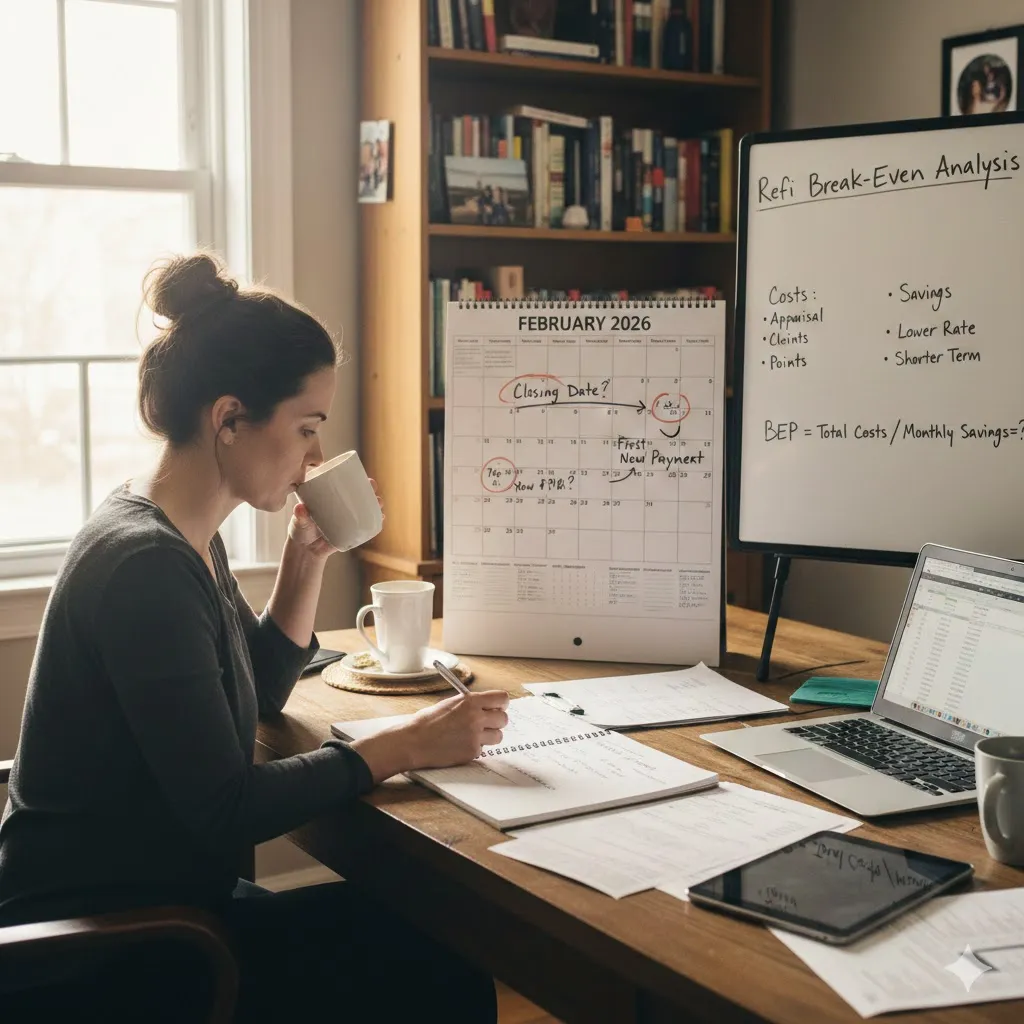

The Break-Even Point That Matters Most

To know if refinancing makes sense, calculate your break-even point—the time it takes for monthly savings to offset closing costs.

For example, if closing costs total $4,000 and your monthly savings are $200, your break-even point is about 20 months. Staying in the home longer than that means real savings.

Disclaimer

This article is for general informational purposes only and does not constitute financial, legal, or mortgage advice. Terms, fees, and eligibility vary. Consult qualified professionals before refinancing.

Pro Insight

The lowest interest rate isn’t always the best refinance. Total loan cost over time—not just the rate—determines true value.

Quick Tip

Ask lenders for a Loan Estimate on the same day to ensure a fair, apples-to-apples comparison.

Frequently Asked Questions

How much are refinance closing costs usually?

They typically range from 2% to 5% of the loan amount, depending on lender and location.

Are refinance closing costs tax-deductible?

Some costs may be deductible over time, but rules vary—consult a tax professional.

Can I negotiate refinance closing costs?

Yes. Some lender fees are negotiable, especially origination charges.

Do no-closing-cost refinances really exist?

Yes, but costs are usually offset through higher rates or loan balances.

Is refinancing worth it if I plan to move?

Often no—unless the break-even point is very short.

Conclusion

Refinance closing costs don’t cancel out the benefits of refinancing—but ignoring them can. When you understand what you’re paying, why you’re paying it, and how long it takes to recover those costs, refinancing becomes a strategic decision rather than a gamble.

Clarity turns fees into facts—and facts lead to smarter financial outcomes.

Trusted U.S. Resources

Consumer Financial Protection Bureau — Refinance Costs

https://www.consumerfinance.gov

U.S. Department of Housing and Urban Development — Refinance Guide

https://www.hud.gov

Federal Reserve — Mortgage Refinancing Basics

https://www.federalreserve.gov