No payday loan alternatives are financial options that help individuals cover urgent expenses without relying on traditional payday loans. Payday loans are known for short repayment timelines and high fees, which has encouraged many borrowers to explore safer borrowing solutions.

Fortunately, several alternatives exist that may offer more manageable repayment structures and lower borrowing costs. These options can help people address temporary financial gaps while maintaining better long-term financial stability.

Understanding these alternatives allows borrowers to make more informed decisions when facing unexpected expenses.

Why Many Borrowers Look for Payday Loan Alternatives

Payday loans are often marketed as fast solutions for urgent financial needs. However, the structure of these loans can create financial strain if repayment deadlines are difficult to meet.

Some reasons people seek alternatives include:

• Short repayment periods tied to the next paycheck

• Higher fees compared with other loan types

• Limited flexibility if repayment becomes difficult

• Potential for repeated borrowing cycles

For these reasons, many financial advisors encourage exploring other borrowing options first.

Common Alternatives to Payday Loans

Several financial products can provide short-term support while offering clearer repayment structures.

Common alternatives include:

• Personal installment loans with fixed monthly payments

• Credit union payday alternative loans (PALs)

• Employer paycheck advances

• Cash advance applications linked to earned wages

These options often provide greater transparency regarding repayment schedules and fees.

Comparing Payday Loan Alternatives

| Option | Key Feature | Typical Borrowing Amount |

|---|---|---|

| Personal installment loan | Fixed repayment schedule | $500 – $5,000+ |

| Payday alternative loan | Credit union program | Up to about $2,000 |

| Paycheck advance | Early access to earned wages | Small amounts |

| Cash advance apps | App-based short-term advance | $20 – $1,500 |

Each alternative works differently depending on eligibility requirements and borrowing needs.

Pro Insight

Financial counselors often recommend exploring credit union products before considering payday loans.

For example, someone facing a sudden $800 car repair might visit a local credit union. Instead of a payday loan requiring full repayment in two weeks, the credit union may offer a payday alternative loan with structured payments over several months.

This type of arrangement can reduce pressure on the borrower’s next paycheck.

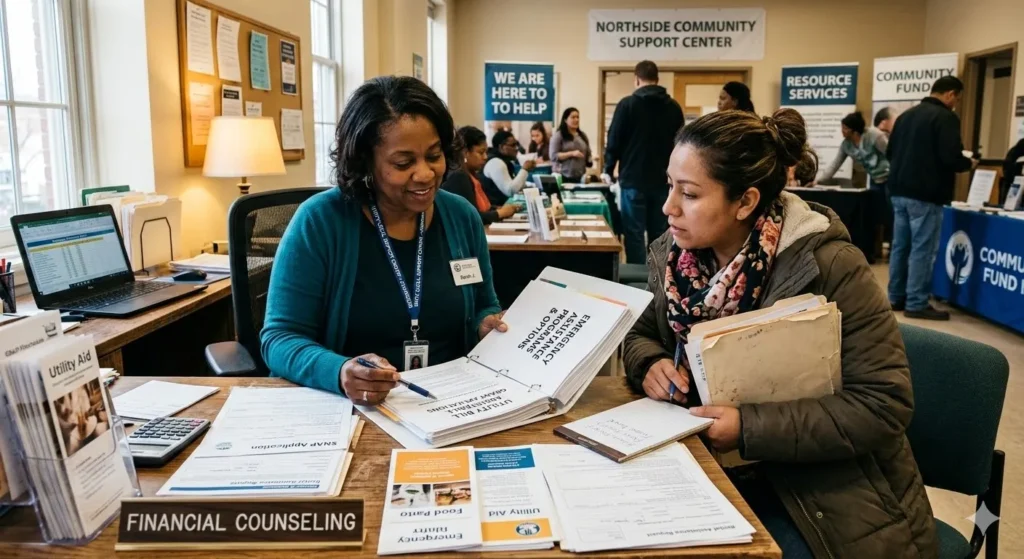

Community and Nonprofit Assistance Programs

Some individuals facing financial hardship may qualify for support programs offered by nonprofit organizations or local agencies.

Examples of assistance include:

• Emergency utility payment programs

• Short-term hardship grants

• Community financial counseling services

• Nonprofit microloan programs

These resources can help address urgent financial needs without requiring high-cost borrowing.

Quick Tip

Before applying for any short-term loan, calculate the total repayment cost, including fees and interest. This helps determine whether the loan fits comfortably within your monthly budget.

Building an Emergency Financial Plan

Many financial advisors encourage building small emergency savings over time to reduce reliance on short-term borrowing.

Even modest savings can help cover smaller unexpected expenses such as appliance repairs or medical copayments.

Over time, this habit may reduce the need for short-term loans entirely.

Frequently Asked Questions

What are payday loan alternatives?

Payday loan alternatives are borrowing or financial assistance options that provide short-term funds without the high fees or short repayment timelines of payday loans.

Are credit union payday alternative loans widely available?

Many credit unions offer payday alternative loans designed to provide small loan amounts with more manageable repayment terms.

Can paycheck advance apps replace payday loans?

Some paycheck advance apps allow workers to access a portion of their earned wages early, which may help cover short-term expenses.

Do personal installment loans work as payday alternatives?

Yes. Personal installment loans allow borrowers to repay funds over time with fixed payments rather than a single lump-sum repayment.

Are there non-loan options for emergency expenses?

Yes. Community assistance programs, payment plans, and financial counseling services may help address urgent financial needs.

Conclusion

No payday loan alternatives provide several options for individuals facing short-term financial challenges. Personal installment loans, credit union programs, paycheck advances, and community assistance services may offer more flexible solutions than traditional payday loans.

By comparing available options and considering repayment terms carefully, borrowers can choose financial solutions that support immediate needs while protecting long-term financial wellbeing.

Trusted U.S. Resources

https://www.consumerfinance.gov

https://www.usa.gov/credit

https://www.federalreserve.gov

https://www.investor.gov

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.