A mortgage qualification calculator helps estimate how much home you can afford based on your income, debt, and financial profile. While it doesn’t replace a lender’s approval, it gives a useful starting point for planning your home purchase.

Understanding how these calculations work can help you set realistic expectations before applying for a loan.

How a Mortgage Qualification Calculator Works

A mortgage qualification calculator uses a few key inputs to estimate your borrowing capacity:

- Gross monthly income

- Monthly debt payments

- Down payment amount

- Interest rate estimate

- Loan term (usually 15 or 30 years)

Based on these, it calculates your maximum affordable monthly payment and estimated loan amount.

Key Factors That Determine Qualification

Lenders rely on similar factors when reviewing applications.

Debt-to-Income Ratio (DTI)

This measures how much of your income goes toward debt.

Credit Score

Higher scores often lead to better loan terms.

Income Stability

Consistent earnings improve approval chances.

Down Payment

Larger down payments can increase borrowing power.

Typical Qualification Benchmarks

| Factor | Common Guideline | Why It Matters |

|---|---|---|

| DTI Ratio | Below 36%–43% | Indicates affordability |

| Credit Score | 620+ (varies) | Affects approval and rates |

| Down Payment | 3%–20% | Reduces lender risk |

| Employment | Stable history | Shows repayment ability |

These benchmarks vary by lender and loan type but provide a general reference.

Pro Insight

Many calculators show the maximum you can borrow, not what you should borrow. Staying below the maximum can provide more flexibility for unexpected expenses and long-term financial comfort.

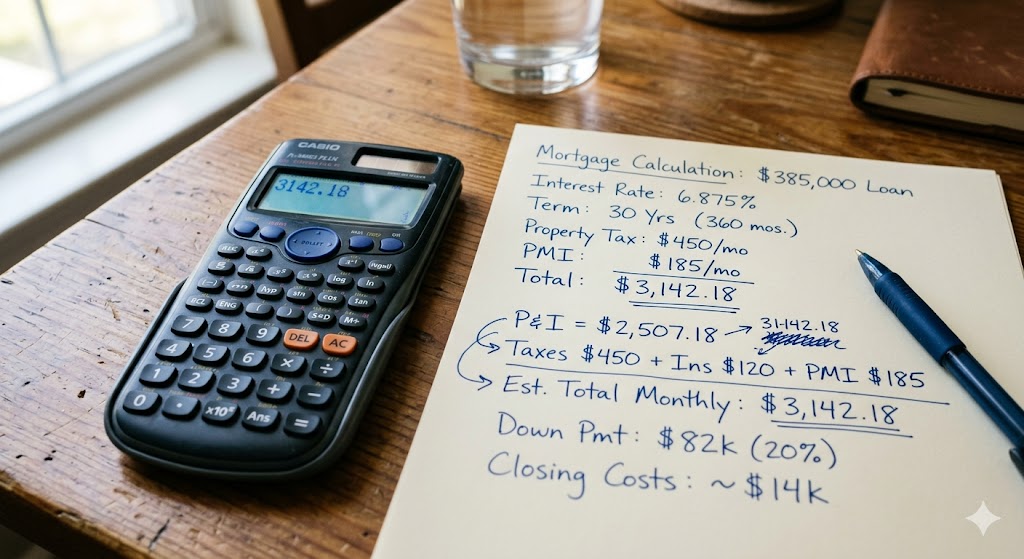

Estimating Your Monthly Payment

A typical mortgage payment includes:

- Principal (loan repayment)

- Interest (cost of borrowing)

- Property taxes

- Homeowners insurance

Some loans also include private mortgage insurance (PMI).

Even if a calculator focuses on principal and interest, your real monthly cost may be higher.

Quick Tip

Use conservative estimates when entering interest rates and expenses. This creates a more realistic view of affordability and avoids surprises later.

Sample Qualification Scenario

Here’s a simplified example:

- Monthly income: $6,000

- Monthly debt: $1,500

- Estimated DTI limit: 40%

Maximum total monthly obligations:

$6,000 × 40% = $2,400

Available for housing:

$2,400 – $1,500 = $900

This suggests a monthly housing budget of around $900, which a calculator would use to estimate a loan amount.

Calculator vs Pre-Approval

| Feature | Calculator | Pre-Approval |

|---|---|---|

| Accuracy | अनुमानित | More precise |

| Credit check | No | Yes |

| Documentation | None | Required |

| Use case | Planning | Buying readiness |

A calculator is a starting point, while pre-approval confirms what a lender is willing to offer.

Common Mistakes When Using Calculators

- Overestimating income stability

- Ignoring additional costs like taxes and insurance

- Using unrealistic interest rate assumptions

- Not accounting for future expenses

- Treating estimates as guaranteed approval

Understanding limitations helps you use the tool more effectively.

How to Improve Your Qualification

- Reduce existing debt

- Increase your credit score

- Save for a larger down payment

- Maintain stable employment

- Avoid new financial obligations before applying

Small improvements can make a noticeable difference in your results.

Frequently Asked Questions

How accurate are mortgage qualification calculators

They provide estimates, but actual approval depends on lender evaluation.

What income should I include

Use your gross (pre-tax) income for most calculations.

Can I qualify with high debt

It depends on your debt-to-income ratio and overall financial profile.

Do calculators include property taxes

Some do, but not all—always check assumptions.

Should I rely only on a calculator

No, it’s best used alongside professional advice and lender pre-approval.

Conclusion

A mortgage qualification calculator is a practical first step in the home buying process. It helps you estimate affordability, understand financial limits, and prepare for conversations with lenders.

While it doesn’t replace formal approval, it provides valuable insight that can guide smarter financial decisions as you move toward homeownership.

Trusted U.S. Resources

https://www.consumerfinance.gov

https://www.hud.gov

https://www.usa.gov/housing

https://www.federalreserve.gov

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.