A mortgage escrow account is a built-in system many lenders use to manage certain homeownership expenses on your behalf. While it may seem like an extra layer in the process, it’s designed to simplify payments and reduce the risk of missed obligations like property taxes or insurance.

What a Mortgage Escrow Account Is

A mortgage escrow account is a separate account managed by your lender. It collects a portion of your monthly payment to cover property-related expenses such as property taxes and homeowners insurance.

Instead of paying these bills separately, you contribute to the escrow account each month. When the bills are due, the lender pays them on your behalf.

This system helps ensure that essential expenses tied to your home are handled consistently and on time.

What Escrow Covers

The escrow portion of your mortgage payment is typically allocated toward specific recurring costs.

Common items include:

- Property taxes

- Homeowners insurance

- Mortgage insurance (if applicable)

- Flood insurance (in certain areas)

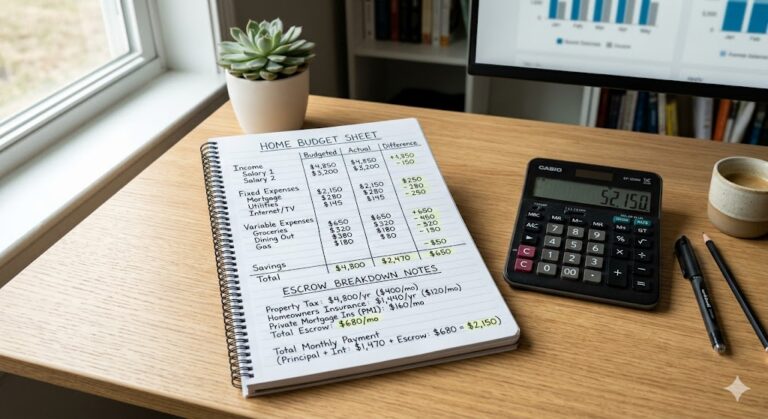

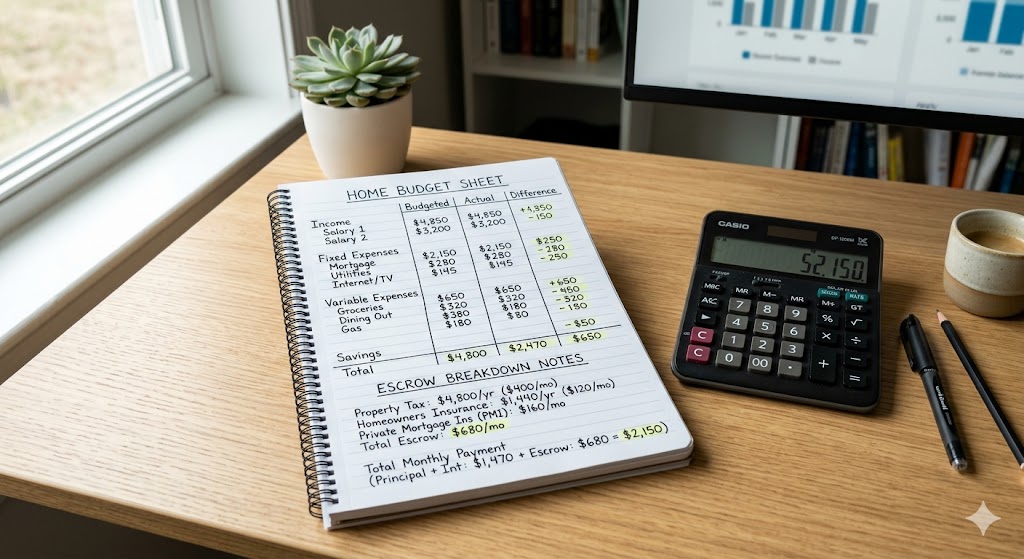

Your monthly mortgage payment is often divided into principal, interest, and escrow—commonly referred to as PITI.

Escrow vs Non-Escrow Mortgages

Not all mortgages require escrow, though many lenders strongly encourage or mandate it.

| Feature | Escrow Account | No Escrow |

|---|---|---|

| Payment Structure | Combined monthly payment | Separate payments |

| Bill Management | Lender handles payments | Homeowner responsible |

| Budgeting | More predictable | Requires planning |

| Flexibility | Less flexible | More control |

Escrow simplifies budgeting, while non-escrow gives you direct control over payments.

How Escrow Payments Are Calculated

Lenders estimate your annual property taxes and insurance costs, then divide that total into monthly installments.

They may also include a small buffer, often called a cushion, to cover potential increases in taxes or insurance premiums.

Each year, your lender performs an escrow analysis. This review compares estimated costs to actual expenses and adjusts your monthly payment if needed.

Pro Insight

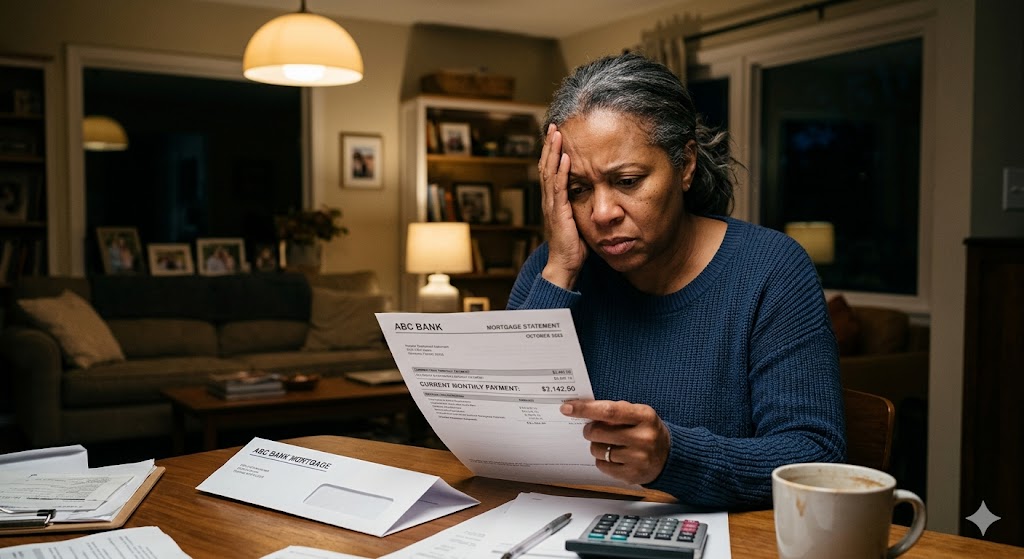

Escrow shortages are common after the first year, especially if property taxes increase. Planning for a possible payment adjustment can help avoid surprises.

Benefits of Using an Escrow Account

Escrow accounts offer several practical advantages.

Simplified payments

Combining expenses into one monthly payment makes budgeting easier.

Reduced risk of missed bills

Your lender ensures taxes and insurance are paid on time.

No large lump-sum payments

Costs are spread throughout the year rather than due all at once.

For many homeowners, this structure adds convenience and peace of mind.

Potential Drawbacks to Consider

Despite the benefits, escrow accounts may not suit everyone.

One limitation is reduced control. You rely on your lender to manage payments and estimates.

Another consideration is fluctuating payments. If taxes or insurance costs rise, your monthly payment can increase.

Additionally, funds in escrow typically do not earn interest for the homeowner, depending on state regulations.

Quick Tip

Review your annual escrow statement carefully. It shows how your funds are used and whether adjustments are needed for the upcoming year.

When Escrow Is Required

Lenders often require escrow accounts in certain situations.

You’re more likely to need escrow if:

- Your down payment is less than 20%

- You have a government-backed loan (like FHA or VA)

- Your lender considers the loan higher risk

If you meet certain criteria later, you may be able to request escrow removal, though approval varies by lender.

Frequently Asked Questions

Is an escrow account mandatory

Not always, but many lenders require it depending on your loan type and down payment.

Can my escrow payment change

Yes, it can increase or decrease based on changes in taxes or insurance costs.

What happens if there’s extra money in escrow

You may receive a refund if the surplus exceeds a certain threshold.

Can I remove my escrow account later

In some cases, yes—if you meet lender requirements and have sufficient equity.

Does escrow include my mortgage payment

No, it’s part of your total payment, but separate from principal and interest.

Conclusion

A mortgage escrow account is designed to make homeownership expenses more manageable by bundling key costs into a single monthly payment. While it may limit some flexibility, it offers convenience and helps ensure important bills are paid on time. By understanding how escrow works and reviewing your statements regularly, you can stay in control of your overall mortgage costs.

https://www.consumerfinance.gov

https://www.hud.gov

https://www.usa.gov

https://www.fanniemae.com

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.