A mortgage affordability calculator helps estimate how much home you can reasonably afford based on your income, expenses, and financial profile. While lenders ultimately determine loan approval, these tools provide a useful starting point for planning a home purchase.

For many buyers in the United States, affordability is not just about the home price—it also includes monthly payments, interest rates, taxes, and insurance. Understanding these factors can help you set a realistic budget before entering the housing market.

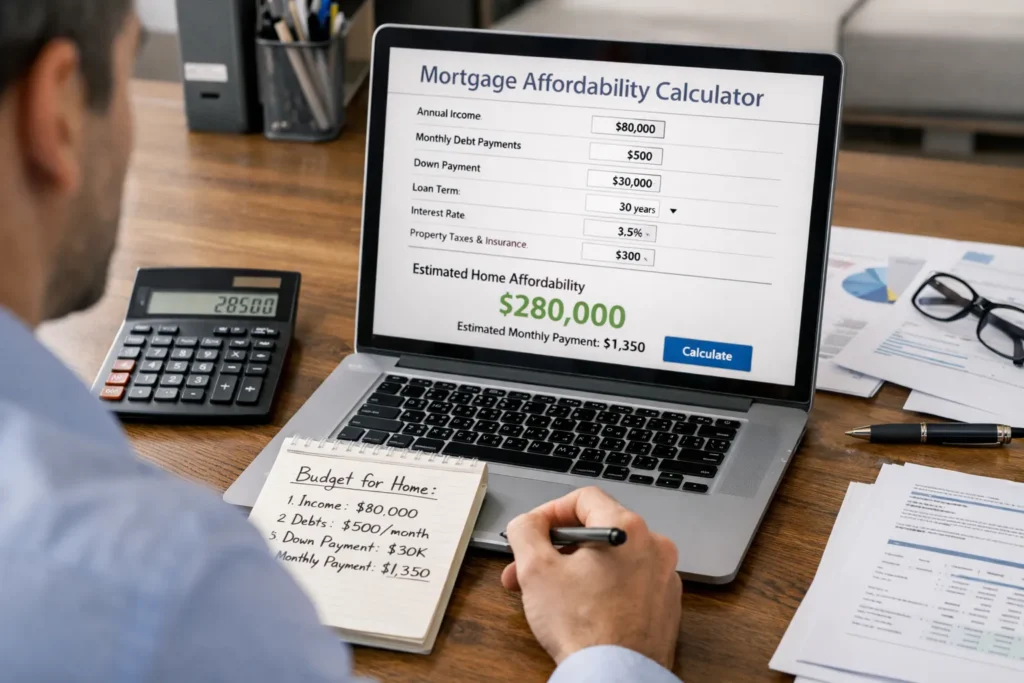

What a Mortgage Affordability Calculator Does

A mortgage affordability calculator estimates your potential home price range based on key financial inputs.

These typically include:

- Gross monthly income

- Monthly debt payments

- Down payment amount

- Interest rate estimate

- Loan term

The calculator uses these inputs to estimate:

- Maximum home price

- Estimated monthly mortgage payment

- Debt-to-income ratio

While the results are not exact, they provide a practical benchmark for planning.

Key Factors That Affect Affordability

Mortgage affordability depends on several interconnected financial elements.

| Factor | How It Affects Affordability |

|---|---|

| Income | Higher income increases borrowing capacity |

| Debt | Higher debt reduces affordability |

| Interest Rate | Higher rates increase monthly payments |

| Down Payment | Larger down payment lowers loan size |

| Loan Term | Longer terms reduce monthly cost |

For example, even a small increase in interest rates can significantly affect monthly payments over time.

Understanding how these factors interact helps explain why affordability varies between borrowers.

The 28/36 Rule Explained

Lenders often use a guideline known as the 28/36 rule when evaluating affordability.

This rule suggests:

- No more than 28% of gross income should go toward housing costs

- No more than 36% of gross income should go toward total debt

For example:

- Monthly income: $6,000

- 28% housing limit: $1,680

- 36% total debt limit: $2,160

These limits help ensure that borrowers can manage mortgage payments alongside other financial obligations.

Example Affordability Scenario

A simple example can illustrate how affordability works.

A buyer earns $5,500 per month and has $500 in existing debt. Using general guidelines, they may be able to afford a monthly housing payment between $1,300 and $1,500.

Based on interest rates and loan terms, this could translate into a home price range depending on:

- Down payment size

- Property taxes

- Insurance costs

This example shows how affordability is tied to both income and existing obligations.

Pro Insight

Mortgage calculators provide estimates, but lenders often include additional costs such as property taxes, homeowners insurance, and private mortgage insurance. Including these in your calculations can lead to a more accurate and realistic budget.

How to Improve Mortgage Affordability

Buyers can take several steps to increase their affordability range.

- Reduce existing debt to improve debt-to-income ratio

- Increase savings for a larger down payment

- Improve credit score for better interest rates

- Compare lenders to find competitive loan terms

Even small improvements in these areas can affect how much home you can afford.

Quick Tip

Before relying on a calculator result, review your full monthly budget. Make sure your estimated mortgage payment leaves room for everyday expenses, savings, and unexpected costs.

Frequently Asked Questions

How accurate are mortgage affordability calculators?

They provide estimates based on the information entered. Actual loan approval and terms may differ depending on lender evaluation.

What income is needed to afford a home?

There is no fixed amount. Affordability depends on income, debt, down payment, and current interest rates.

Do calculators include property taxes and insurance?

Some do, but not all. It’s important to check whether these costs are included in the estimate.

Can I afford a home with existing debt?

Yes, but higher debt reduces borrowing capacity. Lenders use debt-to-income ratios to evaluate this.

Should I get pre-approved after using a calculator?

Yes. Pre-approval provides a more accurate assessment based on verified financial information.

Conclusion

A mortgage affordability calculator is a valuable tool for estimating how much home you can afford before starting the buying process. By considering income, debt, and key financial factors, it provides a realistic starting point for budgeting.

While calculators offer helpful guidance, combining these estimates with lender pre-approval and personal financial planning can lead to more confident and informed homebuying decisions.

Trusted U.S. Resources

https://www.consumerfinance.gov

https://www.hud.gov

https://www.freddiemac.com

https://www.usa.gov

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.