Learn the minimum credit score for a loan, how it varies by loan type, and what lenders really look for beyond the number.

Applying for a loan can feel intimidating—especially when you’re unsure if your credit score is “good enough.” Understanding the minimum credit score for a loan helps you set realistic expectations, avoid unnecessary rejections, and plan smarter next steps.

The truth is, there’s no single magic number. Requirements depend on the loan type, lender, and your overall financial profile.

What Lenders Mean by “Minimum Credit Score”

A minimum credit score is the lowest score a lender is willing to consider for a specific loan. It’s a screening tool, not a guarantee.

For example, two borrowers with the same score may receive different decisions if one has stable income and low debt while the other doesn’t. Lenders look at the full picture, but the score often determines whether your application moves forward.

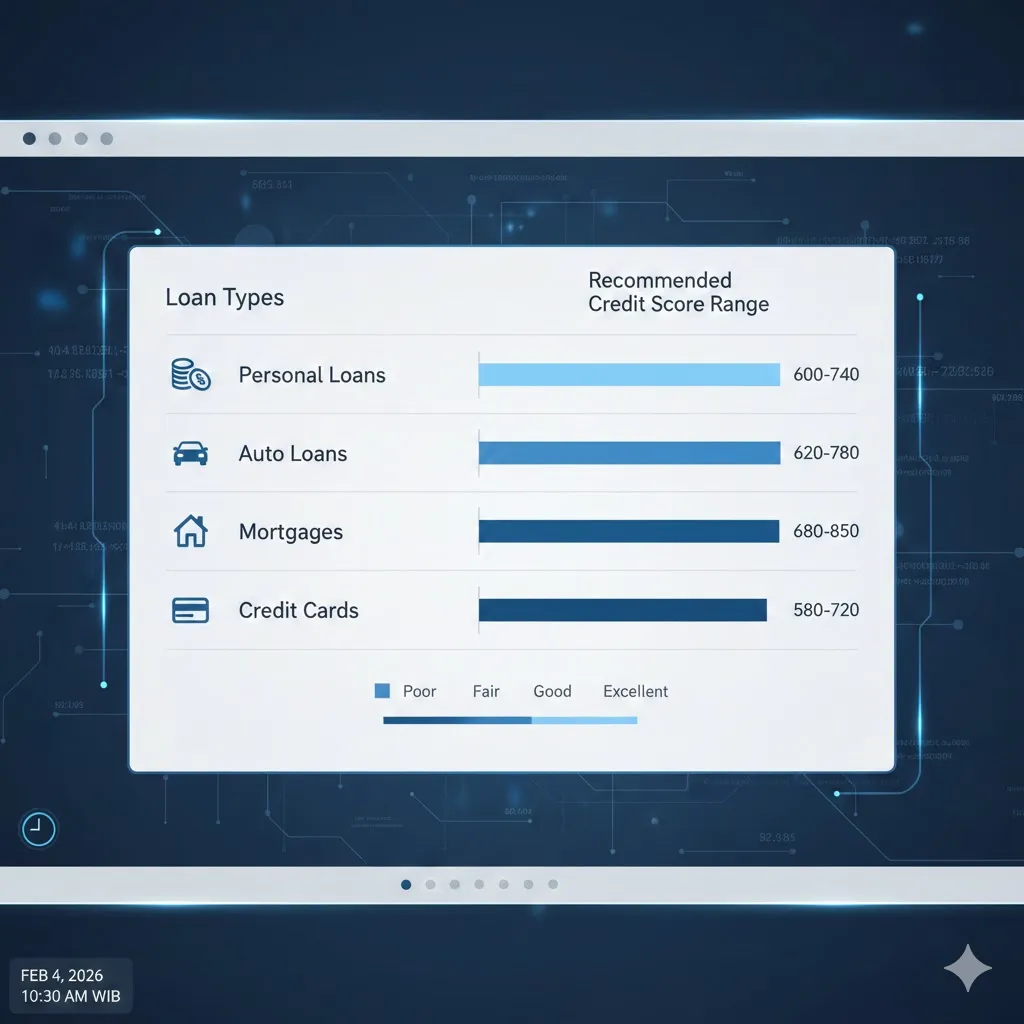

How Minimum Scores Vary by Loan Type

Different loans carry different risk levels, which affects credit score thresholds.

Personal loans and credit cards often require higher scores because they’re unsecured. Auto loans may be more flexible, especially for used vehicles. Mortgages typically have clearer benchmarks set by program guidelines rather than individual lenders.

Understanding which loan fits your current score can save time and frustration.

Minimum Credit Scores Compared by Loan Type

| Loan Type | Typical Minimum Score | Flexibility Level | Notes |

|---|---|---|---|

| Personal loan | 600–660 | Medium | Depends on income and debt |

| Auto loan | 580–620 | High | Dealer financing may vary |

| FHA mortgage | ~580 | High | Lower scores with higher down payment |

| Conventional mortgage | ~620 | Medium | Better terms with higher scores |

| Credit card | 600–700 | Medium | Rewards cards need higher scores |

This comparison shows why knowing the right loan target matters more than chasing a perfect score.

What Matters Besides Your Credit Score

Even if you meet the minimum score, approval isn’t automatic. Lenders also evaluate income stability, debt-to-income ratio, employment history, and recent credit behavior.

A real-life scenario: a borrower with a 610 score but steady income and low debt may be approved, while someone with a 650 score and heavy debt might be declined. Context matters.

That’s why improving overall financial health often matters more than boosting a score by a few points.

How to Improve Approval Odds If Your Score Is Low

If you’re near the minimum, small adjustments can help. Paying down balances, avoiding new credit applications, and correcting errors on your credit report can quickly strengthen your profile.

Some borrowers also choose to apply with a co-signer or wait a few months to show consistent payment history before reapplying.

Disclaimer

This article is for general informational purposes only and does not constitute financial or lending advice. Loan requirements vary by lender and individual circumstances. Always consult qualified professionals before applying.

Pro Insight

Meeting the minimum credit score gets you in the door—but stronger income and lower debt often determine the final decision and interest rate.

Quick Tip

Check your credit score with all three major bureaus before applying—some lenders use specific scoring models.

Frequently Asked Questions

What is the minimum credit score for most loans?

It typically ranges from about 580 to 620, depending on the loan type and lender.

Can I get a loan with a credit score below 600?

Sometimes, yes—especially for auto loans or government-backed mortgages.

Does a higher credit score guarantee approval?

No. Income, debt, and employment also play major roles.

Will applying for a loan hurt my credit score?

A hard inquiry may cause a small, temporary dip, but it’s usually minor.

Should I wait to apply if my score is close to the minimum?

If possible, improving your score and reducing debt can lead to better approval odds and lower rates.

Conclusion

The minimum credit score for a loan is a starting point—not the whole story. While meeting the baseline matters, lenders ultimately care about your ability to repay responsibly.

By understanding score requirements, choosing the right loan type, and strengthening your overall profile, you put yourself in a far better position to get approved on favorable terms.

Trusted U.S. Resources

Consumer Financial Protection Bureau — Credit Scores

https://www.consumerfinance.gov

Federal Trade Commission — Credit Reports

https://www.ftc.gov

U.S. Department of Housing and Urban Development — Mortgage Requirements

https://www.hud.gov