Figuring out how much house you can afford in the USA isn’t just about your income. It’s a combination of debt, credit profile, interest rates, and how comfortably you want to manage monthly payments.

Lenders use formulas to estimate affordability, but smart buyers go a step further—aligning those numbers with real-life expenses and long-term goals.

How Affordability Is Calculated

Most lenders rely on a guideline known as the debt-to-income ratio (DTI). This compares your monthly debt obligations to your gross monthly income.

A commonly used benchmark is the 28/36 rule:

- Up to 28% of income for housing expenses

- Up to 36% for total debt (including loans and credit cards)

Core affordability formula

DTI = \frac{\text{Total Monthly Debt}}{\text{Gross Monthly Income}}

Lower DTI generally improves your borrowing power and loan options.

Key Factors That Affect How Much You Can Afford

Your maximum home price depends on several moving parts.

Income stability

Consistent income carries more weight than occasional spikes.

Existing debt

Car loans, student loans, and credit cards reduce your borrowing capacity.

Down payment

A larger down payment lowers your loan amount and monthly cost.

Interest rates

Even a small rate increase can significantly change affordability.

Property taxes and insurance

These vary by location and must be included in your total payment.

Estimated Affordability by Income

| Annual Income | Estimated Home Price | Monthly Payment Range |

|---|---|---|

| $50,000 | $180,000 – $250,000 | $1,200 – $1,800 |

| $75,000 | $250,000 – $350,000 | $1,700 – $2,400 |

| $100,000 | $320,000 – $450,000 | $2,200 – $3,000 |

| $150,000 | $450,000 – $650,000 | $3,000 – $4,200 |

These are general estimates assuming moderate debt, a standard down payment, and typical interest rates. Actual affordability varies by lender and location.

Pro Insight

Lenders may approve you for more than you’re comfortable spending. Approval limits are based on risk models—not your lifestyle. Many experienced buyers intentionally stay below their maximum to maintain financial flexibility.

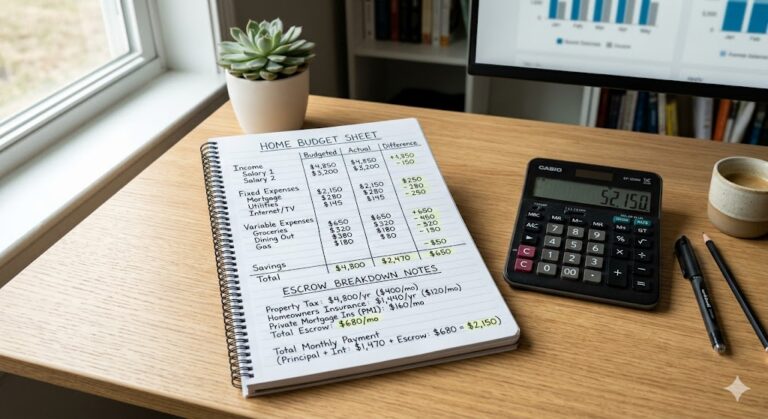

How to Calculate Your Budget Step by Step

A practical approach often works better than relying only on lender estimates.

1. Start with monthly income

Use your take-home pay, not just gross income.

2. Subtract fixed expenses

Include debt payments, utilities, groceries, and savings.

3. Estimate housing costs

Include mortgage, taxes, insurance, and maintenance.

4. Stress-test your budget

Ask whether the payment still feels manageable with unexpected expenses.

Quick Tip

Aim for a monthly housing payment that still allows room for savings and emergencies. A home should support your financial life—not restrict it.

Real-World Micro Scenario

A buyer earning $90,000 annually gets approved for a $400,000 home. After reviewing their monthly budget, they realize the payment would limit savings and travel plans.

Instead, they choose a $320,000 home—keeping monthly costs lower and maintaining financial breathing room.

That decision often leads to less stress over time.

Hidden Costs Many Buyers Overlook

Affordability goes beyond the mortgage itself.

Maintenance and repairs

Homes require ongoing upkeep, often 1–2% of property value annually.

Closing costs

Typically range from 2% to 5% of the home price.

HOA fees

Common in condos or planned communities.

Property taxes

Can vary significantly depending on the state and county.

Ignoring these can stretch your budget more than expected.

Frequently Asked Questions

How much house can I afford based on my salary?

Most buyers can afford a home priced at about 3 to 5 times their annual income, depending on debt and down payment.

What is a safe mortgage payment percentage?

Many financial guidelines suggest keeping housing costs below 28% of gross monthly income.

Does a higher down payment increase affordability?

Yes, it reduces your loan amount and monthly payments, improving overall affordability.

How does credit score affect home affordability?

Higher credit scores often lead to better interest rates, which can increase your purchasing power.

Can I afford a house with high debt?

It’s possible, but higher debt reduces your borrowing capacity and may increase financial strain.

Conclusion

Determining how much house you can afford in the USA is part calculation, part personal decision. While lenders provide a starting point, your comfort level and long-term goals should guide the final number.

A well-balanced budget—one that accounts for both expected and unexpected costs—can make homeownership more sustainable and less stressful.

Trusted U.S. Resources

https://www.consumerfinance.gov

https://www.hud.gov

https://www.fanniemae.com

https://www.freddiemac.com

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.