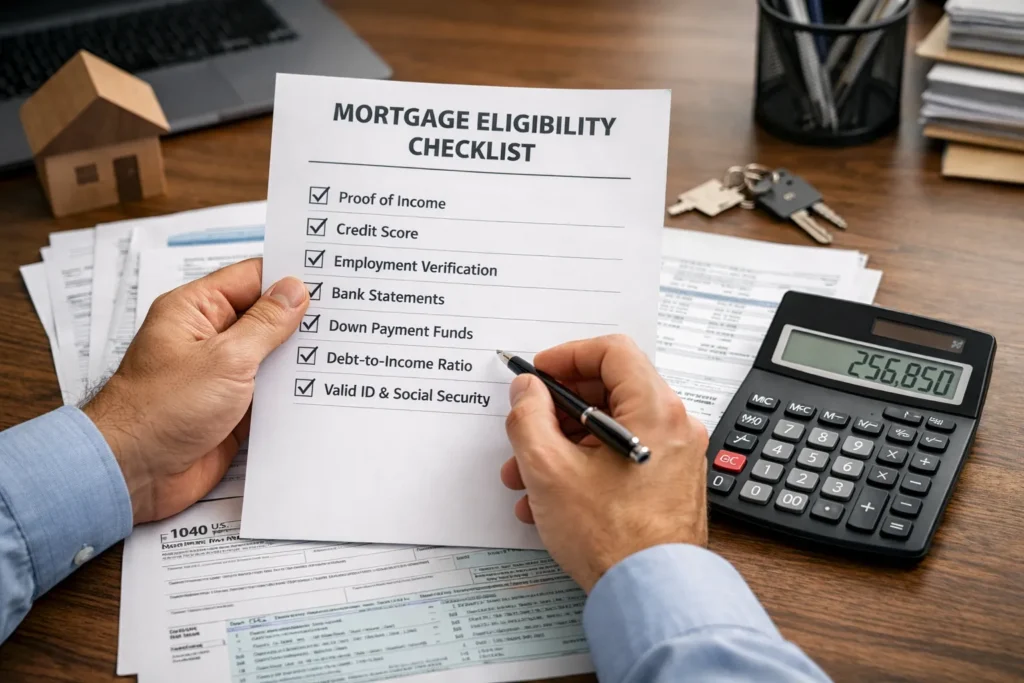

Qualifying for a home loan in the United States depends on a combination of financial factors rather than a single requirement. Lenders evaluate your overall ability to repay the loan by reviewing credit, income, debt, and savings.

For most borrowers, understanding home loan eligibility early can make the buying process smoother and improve the chances of approval. Different loan programs also have different requirements, which gives flexibility depending on your financial situation.

What Determines Home Loan Eligibility

Lenders use a set of core criteria to determine whether you qualify for a mortgage.

Key factors include:

- Credit score

- Income and employment history

- Debt-to-income ratio (DTI)

- Down payment and savings

- Property type and value

These elements are reviewed together to assess your financial stability and repayment ability.

No single factor guarantees approval, but stronger overall financial profiles improve eligibility.

Credit Score Requirements by Loan Type

Your credit score plays a major role in mortgage eligibility and loan terms.

| Loan Type | Typical Minimum Credit Score |

|---|---|

| Conventional Loan | ~620+ |

| FHA Loan | 500–580+ |

| VA Loan | No official minimum (lenders often ~620) |

| USDA Loan | ~640 preferred |

For example, FHA loans may allow scores as low as 500, but require higher down payments at lower scores.

Conventional loans typically require at least 620, with higher scores improving approval chances and interest rates.

Income and Employment Requirements

Lenders want to see stable and reliable income over time.

Common expectations include:

- At least 2 years of consistent employment history

- Verifiable income through pay stubs, tax returns, or bank statements

- Stable or increasing earnings

There is no fixed income level required. Instead, lenders compare your income to your debts and loan amount.

Debt-to-Income Ratio Explained

Debt-to-income ratio (DTI) measures how much of your income goes toward debt payments.

- Ideal DTI is typically 43% or lower

- Some programs may allow higher ratios with strong financial factors

For example:

- Income: $6,000/month

- Debt: $2,400/month

- DTI: 40%

Lower DTI ratios generally improve eligibility and loan terms.

Down Payment Requirements

Your down payment affects both eligibility and loan cost.

| Loan Type | Minimum Down Payment |

|---|---|

| Conventional | ~3% |

| FHA | 3.5% (580+ credit score) |

| FHA (lower credit) | 10% |

| VA / USDA | 0% (eligible borrowers) |

For FHA loans, a 3.5% down payment is possible with a 580+ credit score, while lower scores require more upfront funds.

Higher down payments can improve approval chances and reduce monthly costs.

Pro Insight

Lenders often evaluate your application as a complete financial picture. A borrower with a slightly lower credit score may still qualify if they have strong income, low debt, and a larger down payment.

Balancing multiple strengths can significantly improve eligibility.

Additional Eligibility Factors

Beyond the main criteria, lenders may also review:

- Savings and cash reserves

- Property appraisal results

- Loan purpose (primary residence vs investment)

- Payment history and credit behavior

For government-backed loans like FHA, the property must also meet certain safety and condition standards.

Quick Tip

Before applying, avoid taking on new debt such as credit cards or auto loans. Changes in your financial profile can affect eligibility during the approval process.

Frequently Asked Questions

What is the minimum credit score to qualify for a mortgage?

Many conventional loans require around 620, while FHA loans may allow scores as low as 500 depending on the down payment.

How much income do you need to qualify?

There is no fixed amount. Lenders evaluate income relative to debts using the debt-to-income ratio.

Can you qualify for a home loan with low credit?

Yes. Government-backed loans like FHA are designed to help borrowers with lower credit scores qualify.

Is a down payment always required?

Most loans require a down payment, but VA and USDA loans may offer zero down for eligible borrowers.

How long does it take to get approved?

The process typically takes several weeks, depending on documentation and lender review.

Conclusion

Home loan eligibility in the United States is based on a combination of financial factors, including credit score, income stability, debt levels, and available savings. Different loan programs provide flexibility, allowing borrowers with varying financial profiles to qualify.

By understanding these requirements and preparing in advance, borrowers can improve their chances of approval and secure more favorable loan terms.

Trusted U.S. Resources

https://www.hud.gov

https://www.consumerfinance.gov

https://www.freddiemac.com

https://www.usa.gov

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.