Learn the difference between hard inquiry vs soft inquiry, how each impacts your credit score, and when they occur.

When checking your credit, not all inquiries are created equal. Understanding hard inquiry vs soft inquiry helps you protect your credit score, plan applications wisely, and avoid unnecessary drops that catch many people off guard.

Both types involve reviewing your credit report—but their impact and purpose are very different.

What a Credit Inquiry Really Is

A credit inquiry happens when someone accesses your credit report. Lenders, employers, insurers, and even you can trigger inquiries depending on the situation.

The key difference lies in why your credit is being checked and who initiated it. One type can affect your score. The other won’t touch it at all.

What Is a Hard Inquiry?

A hard inquiry occurs when you apply for new credit and a lender reviews your credit to make an approval decision.

Common situations that trigger hard inquiries include applying for a credit card, personal loan, auto loan, or mortgage. Because hard inquiries signal potential new debt, they can slightly lower your credit score.

A real-life scenario: applying for multiple credit cards in a short time can stack hard inquiries, making lenders view you as higher risk—even if you’re approved.

Hard inquiries typically stay on your credit report for up to two years, but their score impact usually fades within a few months.

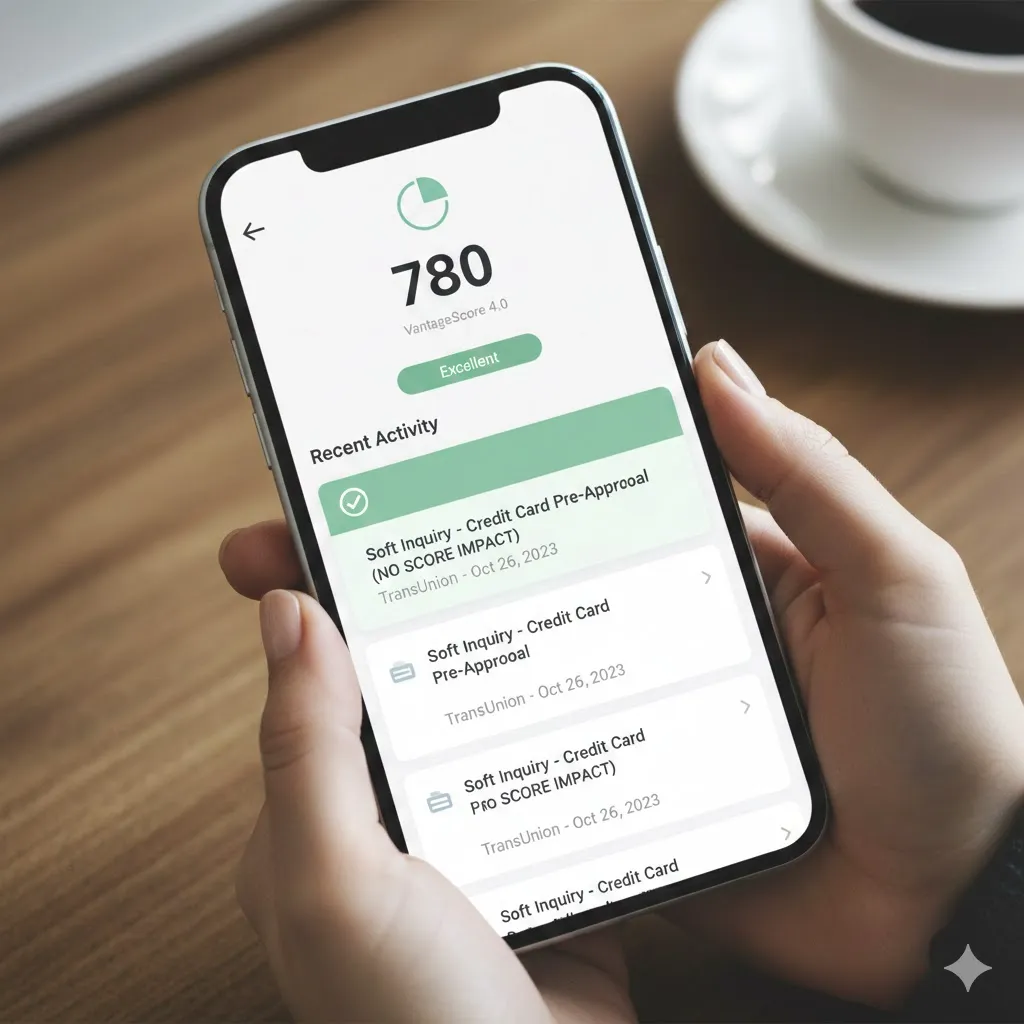

What Is a Soft Inquiry?

A soft inquiry happens when your credit is checked for informational or background purposes.

Examples include checking your own credit score, pre-approval offers, employer background checks, or account reviews by existing lenders. Soft inquiries are invisible to lenders and never affect your credit score.

You could have dozens of soft inquiries without any negative impact.

Hard Inquiry vs Soft Inquiry Compared

| Feature | Hard Inquiry | Soft Inquiry |

|---|---|---|

| Affects credit score | Yes (slightly) | No |

| Visible to lenders | Yes | No |

| Requires application | Yes | No |

| Typical duration | Up to 2 years | Informational only |

| Examples | Loans, credit cards | Credit checks, pre-approvals |

This comparison makes it clear why knowing the difference matters before applying for credit.

How Inquiries Affect Real Credit Decisions

One hard inquiry usually isn’t a problem. Several in a short period can be.

For example, rate-shopping for a mortgage within a short window is often treated as a single inquiry for scoring purposes. But spreading applications over months can multiply the impact.

Understanding this timing helps you apply strategically rather than reactively.

Disclaimer

This article is for general informational purposes only and does not constitute financial or credit advice. Credit scoring models and lender practices vary. Review your personal situation carefully.

Pro Insight

Lenders care less about one inquiry and more about patterns. Multiple hard inquiries in a short time can raise red flags faster than a single low score.

Quick Tip

Always check whether an application involves a hard inquiry before submitting—many pre-approvals use soft inquiries only.

Frequently Asked Questions

Does checking my own credit cause a hard inquiry?

No. Personal credit checks are always soft inquiries.

How many hard inquiries are too many?

There’s no fixed number, but several within a few months can impact approval odds.

Do soft inquiries show on my credit report?

Yes, but only you can see them—lenders cannot.

How much does a hard inquiry lower my score?

Usually a few points, and the effect is temporary.

Can I remove hard inquiries?

Only if they’re incorrect or unauthorized; legitimate inquiries remain.

Conclusion

Understanding hard inquiry vs soft inquiry gives you control over one of the simplest yet most misunderstood credit factors. Soft inquiries are harmless. Hard inquiries matter—but only when overused.

By applying strategically and knowing what triggers each type, you protect your credit score while still accessing the financial tools you need.

Trusted U.S. Resources

Consumer Financial Protection Bureau — Credit Reports

https://www.consumerfinance.gov

Federal Trade Commission — Credit Inquiries

https://www.ftc.gov

FICO — Credit Score Factors

https://www.myfico.com