Buying your first home in the United States is a major milestone, but it also involves a series of financial and practical decisions. From preparing your budget to closing the deal, each step plays a role in shaping your long-term experience as a homeowner.

A clear, structured approach can help you move forward with confidence and avoid common setbacks.

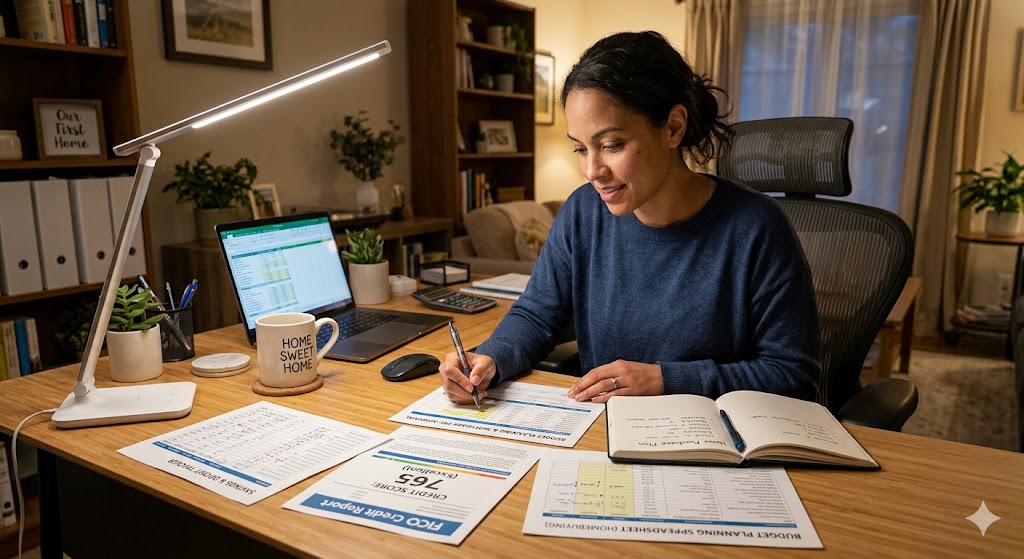

Preparing Financially Before You Buy

Before looking at homes, it’s important to understand your financial position.

Key steps include:

- Reviewing your credit score and history

- Calculating your debt-to-income ratio

- Building savings for down payment and closing costs

- Setting a realistic monthly housing budget

A strong financial foundation improves your loan options and reduces stress later in the process.

Understanding Your Total Budget

Many buyers underestimate the full cost of homeownership.

A simple way to estimate:

Monthly\ Cost = Mortgage + Taxes + Insurance + Maintenance

In addition to your mortgage, consider:

- Property taxes (vary by location)

- Homeowners insurance

- Maintenance and repairs

- Utilities and HOA fees (if applicable)

Looking beyond the purchase price helps prevent overextending your finances.

Getting Pre-Approved for a Mortgage

Pre-approval is one of the most important early steps.

It involves:

- A lender reviewing your financial profile

- Determining how much you can borrow

- Providing a pre-approval letter for sellers

Benefits include:

- Clear price range

- Stronger position when making offers

- Faster closing process

Pre-approval also helps you identify any issues before house hunting begins.

Finding the Right Home

Once pre-approved, you can start searching for homes that match your needs.

Consider:

- Location and commute

- Neighborhood characteristics

- Home condition and age

- Future resale potential

It’s helpful to create a checklist of priorities to stay focused during your search.

Making an Offer and Negotiating

When you find a home, the next step is submitting an offer.

This process may include:

- Setting a competitive price

- Including contingencies (inspection, financing)

- Negotiating terms with the seller

In competitive markets, flexibility and preparation can make a difference.

Pro Insight

First-time buyers often focus heavily on the purchase price but overlook negotiation opportunities. Closing costs, repairs, or seller concessions can sometimes be adjusted to improve your overall deal.

Home Inspection and Appraisal

After your offer is accepted:

- A home inspection evaluates the property’s condition

- An appraisal determines the home’s market value for the lender

These steps help confirm that the home is worth the price and identify potential issues.

Closing the Deal

Closing is the final step where ownership transfers.

It typically involves:

- Signing legal documents

- Paying closing costs

- Finalizing your mortgage

Once completed, you receive the keys and officially become a homeowner.

Quick Tip

Keep extra funds available after closing. Unexpected repairs or setup costs often arise within the first few months of ownership.

Common Mistakes to Avoid

- Skipping pre-approval before house hunting

- Underestimating total monthly costs

- Draining all savings for the down payment

- Ignoring inspection findings

- Making large financial changes before closing

Avoiding these mistakes can make the process smoother and more manageable.

Frequently Asked Questions

How much do I need for a first home purchase

It varies, but many buyers put down 3%–20% plus closing costs.

How long does the home buying process take

Typically 30 to 60 days after an offer is accepted.

What credit score is needed to buy a home

Requirements vary, but many programs accept scores starting around the low 600s.

Should I use a real estate agent

Many buyers find agents helpful for navigating negotiations and paperwork.

What are closing costs

They include fees for the loan, appraisal, title services, and other expenses.

Conclusion

Buying your first home in the USA involves careful planning, from financial preparation to closing day. By understanding each step—budgeting, financing, searching, and finalizing—you can approach the process with greater clarity and confidence.

A well-informed buyer is better equipped to make decisions that support both immediate needs and long-term financial stability.

Trusted U.S. Resources

https://www.hud.gov

https://www.consumerfinance.gov

https://www.usa.gov

https://www.fanniemae.com

This article is for general informational purposes only and does not provide legal, financial, medical, or professional advice. Policies, rates, and regulations may change over time.