A clear guide to FHA down payment percentage, how it works, and what buyers need to qualify in the U.S. housing market.

Understanding the FHA down payment percentage can be the difference between renting forever and finally owning a home. Thanks to the Federal Housing Administration (FHA), many Americans—especially first-time buyers—can secure a mortgage with a smaller upfront cost than conventional loans.

In 2026, when housing prices remain high and saving is challenging, FHA loans continue to be one of the most accessible paths to homeownership for buyers with modest savings and varied credit histories.

What FHA Down Payment Percentage Really Means

An FHA loan is a government-insured mortgage designed to help borrowers who might not qualify for traditional financing. One of its biggest benefits is the lower down payment requirement compared with conventional loans.

Instead of saving 10–20% of a home’s price, FHA loans allow many buyers to put down significantly less.

Here’s how the down payment percentages typically work:

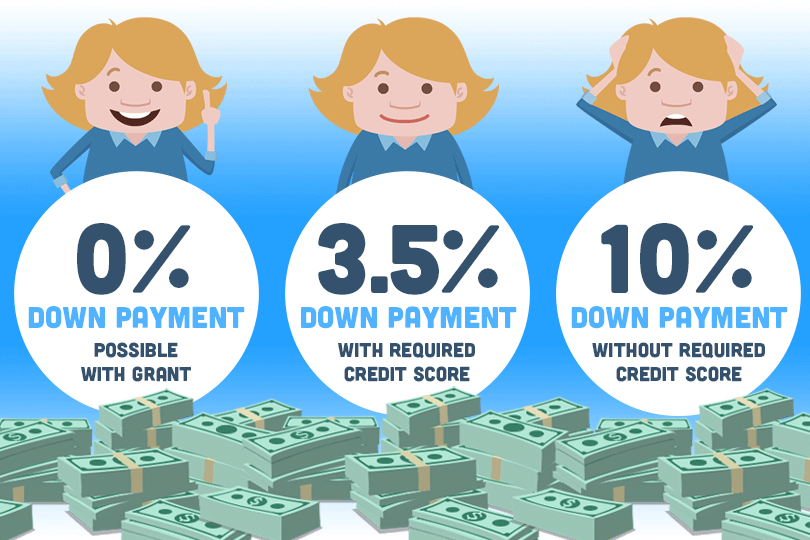

- 3.5% Down Payment:

Available for borrowers with a credit score of 580 or higher. This is the most common FHA down payment threshold. - 10% (or more) Down Payment:

Required for borrowers with credit scores between 500 and 579, though many lenders also have overlays (stricter requirements).

These percentages apply to the purchase price or appraised value, whichever is lower.

Why 3.5% Is Significant for Buyers

A 3.5% down payment can dramatically reduce the cash needed upfront. For example:

- On a $300,000 home, a 3.5% down payment is $10,500, compared with $60,000 for a 20% conventional down payment.

This small upfront cost helps buyers enter the housing market sooner, especially in competitive areas where waiting years to save more isn’t practical.

However, FHA loans come with mortgage insurance premiums (MIP) that remain part of the monthly payment, so total costs require careful budgeting.

Who Qualifies for the Lower FHA Down Payment

Qualifying for a 3.5% down payment isn’t automatic—it depends on your financial profile.

Key Qualification Factors:

- Credit score: 580 or higher for 3.5% down

- Steady income: Verifiable employment and income

- Debt-to-income ratio (DTI): Acceptable by lender guidelines

- Primary residence: FHA loans require owner occupancy

If you have a lower credit score (500–579), you may still qualify, but you’ll likely need a 10% down payment and a solid track record demonstrating responsibility with credit and debt.

FHA Down Payment vs Conventional Loan Down Payment

| Loan Type | Typical Down Payment | Credit Score Guidance | Mortgage Insurance |

|---|---|---|---|

| FHA Loan | 3.5% (580+) | 580+ for 3.5%, 500–579 for 10%+ | Yes, required |

| Conventional Loan | 5–20%+ | 620+ commonly required | PMI if <20% |

This comparison helps buyers choose the path that makes sense for their situation and readiness.

Tips for Managing FHA Down Payment Requirements

Putting together even a 3.5% down payment can feel daunting. Some strategies that many buyers consider include:

- Down Payment Assistance Programs: State and local programs often offer help for qualified buyers.

- Gifts from Family: FHA allows down payment gifts from eligible sources when properly documented.

- Savings Plans: Automating savings and trimming discretionary expenses can accelerate progress.

Disclaimer

This article is for informational purposes only and does not constitute financial, legal, or mortgage advice. Loan requirements vary by lender, income, credit, and local guidelines.

Pro Insight

While 3.5% is a big advantage, always run the numbers on total monthly payments, including mortgage insurance, property taxes, and insurance, to ensure long-term affordability.

Quick Tip

Check multiple lenders—FHA loan terms, fees, and overlays can vary significantly from one lender to another.

Common Misunderstandings About FHA Down Payments

A frequent misconception is that FHA down payment is “no money down.” It is not. You still need cash at closing—sometimes more than just the down payment—to cover closing costs.

Another misunderstanding is that FHA loans are only for first-time buyers. In reality, FHA loans are available to repeat buyers who meet requirements.

FAQs About FHA Down Payment Percentage

Is 3.5% down always available?

Yes if you meet credit and income qualifications; otherwise, higher down payments may be required.

Can I use gift funds for an FHA down payment?

Yes, FHA allows down payment gifts if properly documented by the donor.

Does FHA require mortgage insurance?

Yes. FHA loans require both upfront and ongoing mortgage insurance premiums (MIP).

Can I avoid mortgage insurance with an FHA loan?

No. FHA mortgage insurance is required for the life of the loan unless you refinance into a conventional loan.

Is the FHA down payment based on purchase price or appraisal?

It’s based on the lower of the two—purchase price or appraised value.

Conclusion

The FHA down payment percentage—most often **3.5% for qualified buyers—is one of the most powerful tools for first-time and budget-conscious homebuyers in the United States. While it doesn’t eliminate all costs or risks, it significantly lowers the barrier to entry.

With clear understanding, realistic budgeting, and exploration of assistance options, many buyers find that FHA loans turn homeownership from a distant goal into a practical next step.

U.S. Trusted Resources

- U.S. Department of Housing and Urban Development (FHA Loan Info)

https://www.hud.gov - Consumer Financial Protection Bureau – Buying a Home Guide

https://www.consumerfinance.gov - Federal Housing Administration – FHA Mortgage Requirements

https://www.hud.gov/federal_housing_administration - U.S. Small Business Administration – Homeownership Tools

https://www.sba.gov