Auto loan interest rate USA shapes how much you really pay for a car—not just the sticker price. In 2026, rates vary widely based on your credit profile, lender type, loan term, and market conditions. Knowing how these pieces fit together helps you negotiate better terms and avoid long-term cost surprises.

This guide focuses on real factors that determine your auto loan interest rate—not just published ads.

This article is for general informational purposes only and does not provide financial, legal, or lending advice. Loan offers, rates, and terms vary by lender, credit profile, location, and market conditions.

Why auto loan interest rates matter

A lower interest rate doesn’t just reduce monthly payments—it reduces the total cost of ownership. Even a few percentage points can cost you hundreds or thousands over the life of the loan.

For example, two drivers in Ohio bought identical vehicles. One qualified for 6% APR; the other, with slightly weaker credit, paid 11%. Over a 60-month loan, the difference added up to thousands more in interest paid.

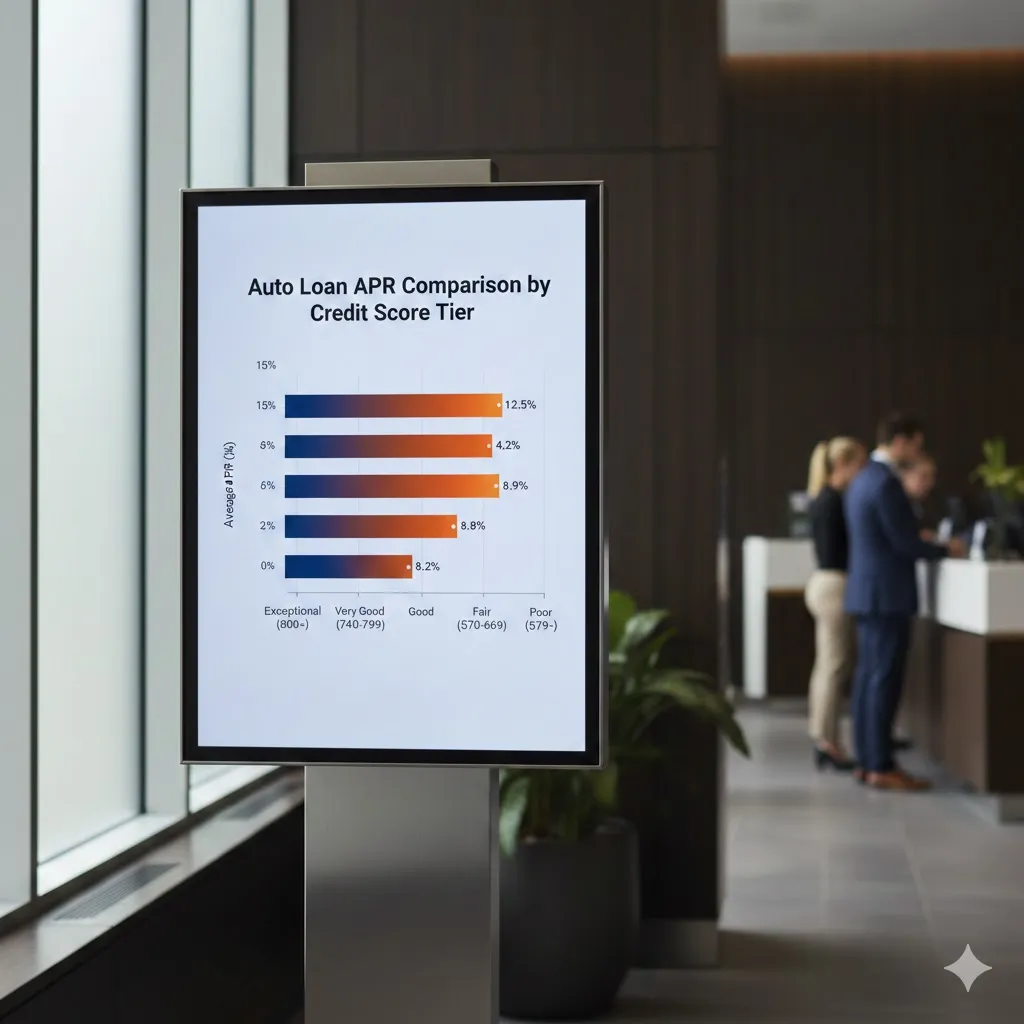

Typical auto loan interest rate ranges in the U.S.

Auto loan rates aren’t a single number—they’re a range. In 2026, typical APR ranges approximate:

| Credit Tier | Approx. APR Range* | Notes |

|---|---|---|

| Excellent (750+) | ~4%–7% | Best pricing |

| Good (700–749) | ~6%–10% | Competitive |

| Fair (650–699) | ~9%–14% | Higher cost |

| Poor (600–649) | ~12%–20% | Risk pricing |

| Subprime (<600) | 18%+ | Limited options |

*Actual rates vary by lender, loan term, new vs. used vehicles, and market conditions.

What actually influences your rate

Auto loan pricing reflects risk and market conditions. Key factors include:

Credit Score

This is often the most visible factor brands refer to. Higher scores usually unlock lower APRs.

Loan Term

Shorter terms (36–48 months) usually have lower rates than extended terms (60–72+ months).

Vehicle Type

New cars often qualify for lower rates than used cars, but certified pre-owned vehicles may bridge the gap.

Down Payment

A larger down payment lowers the financed amount and reduces lender risk, often improving pricing.

Lender Type

Credit unions, banks, and online lenders each price differently (see comparison below).

If your site includes credit score education or budgeting guides, internal linking fits naturally here.

Comparing lenders for auto loans

Different lenders serve different borrower profiles.

| Lender Type | Typical Rate Range | Best For | Notes |

|---|---|---|---|

| Credit unions | ~4%–12% | Strong members | Often lower for loyal members |

| Online lenders | ~5%–15% | Quick approvals | Competitive for strong profiles |

| Banks | ~6%–14% | Existing customers | Moderate pricing |

| Dealer financing | ~7%–20% | Convenience | Often higher unless promotional |

Pro Insight

Prequalification tools that use soft credit checks let you see realistic rate ranges without hurting your credit score. Use them before applying for full approval.

Quick Tip

If your initial offer seems high, ask the lender if they’ll match a competitor’s better rate. Many borrowers secure better pricing simply by showing competing prequalified offers.

When rates can change

Auto loan interest rates can shift due to:

- Federal Reserve rate moves

- General credit market conditions

- Seasonal promotions from dealers

- Changes in your credit score between inquiry and application

If rates rise between your prequalification and final application, ask the lender how to secure the earlier pricing or re-prequalify.

FAQs

What is a good auto loan interest rate in the U.S.?

Rates under ~7% are generally competitive for buyers with strong credit in 2026.

Do used cars cost more to finance?

Often yes — used vehicles typically carry higher APRs due to depreciation and risk.

Does my income matter for auto loan rates?

Yes. Lenders assess income stability alongside credit score.

Can I refinance an auto loan to lower my rate?

Yes. Refinancing can reduce your rate if your credit improves.

Will applying to multiple lenders hurt my credit?

Soft prequalification checks don’t. Multiple hard inquiries can affect your score slightly.

Conclusion

Understanding how auto loan interest rate USA works helps you shop smarter—not just at the dealership, but across lenders. Your credit profile, loan term, vehicle age, and lender type all shape the APR you actually pay. By comparing offers, prequalifying strategically, and negotiating based on data, you can lower your total cost and drive away with both confidence and savings.

Trusted U.S. Resources

- Consumer Financial Protection Bureau (CFPB): https://www.consumerfinance.gov

- Federal Trade Commission (FTC) Auto Loans: https://www.ftc.gov

- Federal Reserve Consumer Guides: https://www.federalreserve.gov